Do you know that most insurance providers (in the US) cover post-mastectomy bras for women who have undergone a mastectomy? There are limitations, deductibles and co-pays still apply, and you might have to jump through some hoops. More info below photos.

I get six bras and six camisoles per year under my current plan. I recently visited a local mastectomy boutique for a fitting and left with four Coobie bras, two Anita bras, and two camisoles (+ third on order). I will return in the spring when Amoena releases new colors and styles to pick up three more camisoles. The experience was relatively hassle-free and since I already met my out-of-pocket maximum for the year, they were all covered at 100%.

How does it work?

I started by calling my insurance provider to check level of coverage and to request a list of providers. Post-mastectomy bras are considered medical devices (the code is L8000), so I got a list of places that sell all kinds of devices, which didn’t really help. Then I contacted a local mastectomy boutique: 1. to ask if they work with my insurance provider, 2. determine what I needed to do before I came in, and 3. to make an appointment. I provided my surgeon’s contact information and my insurance details. The boutique reached out to my plastic surgeon and obtained the required prescription and details. They also contacted my insurance provider and secured pre-authorization. A week later I got a call that all was set. They really made it easy.

Some insurance providers work with stores like Nordstrom (appointment required). Those that don’t may reimburse after the fact. Also, stores carry different stock, so if you want Coobie bras, you may need to call around. Keep looking until you find a place that works for you. There are options. Nordstrom will even remove underwires for free (so I hear).

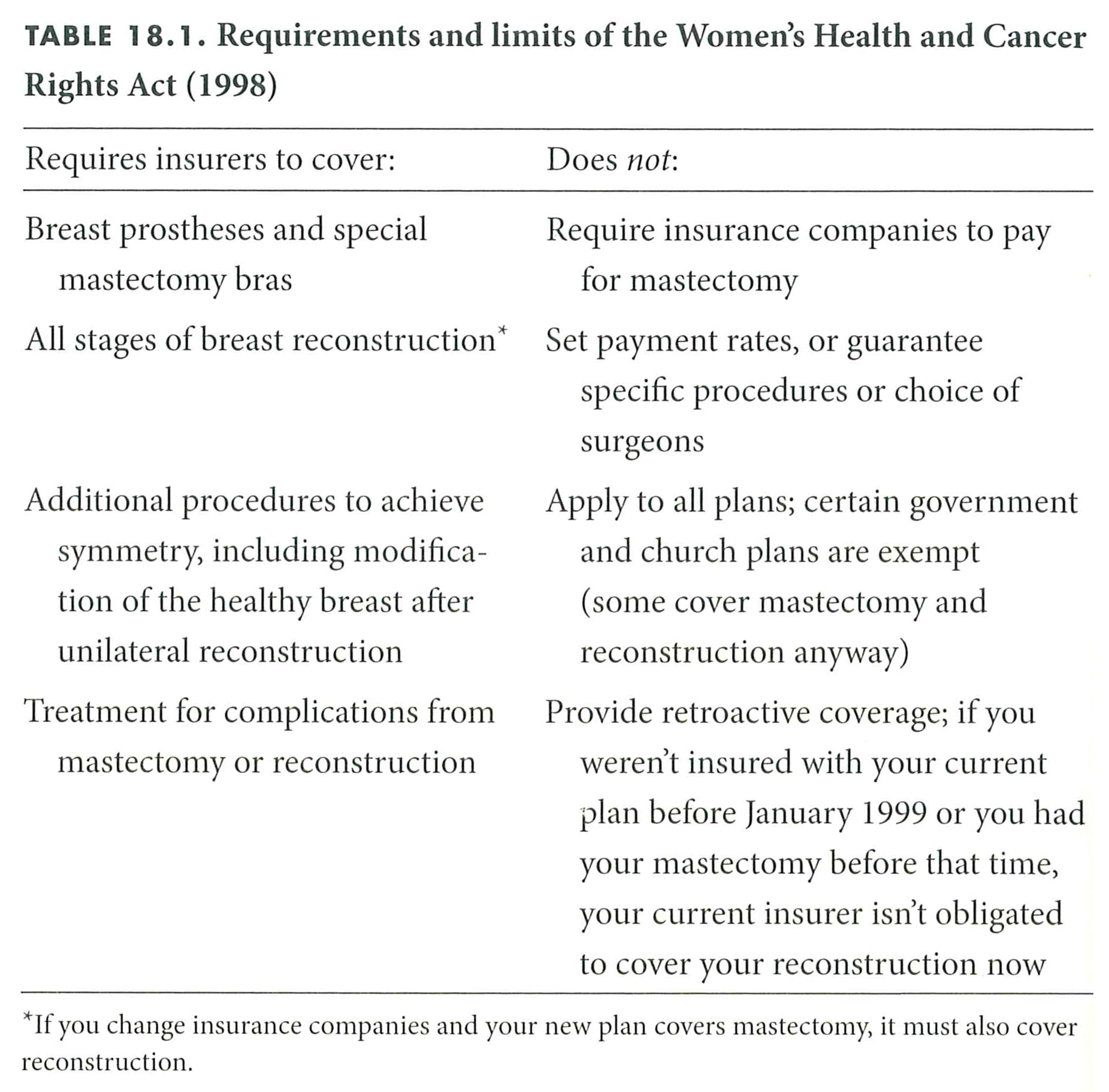

There are providers out there that post their policy online and you may see caveats such as “covered instead of reconstructive breast surgery” or that a breast cancer diagnosis is required. Don’t give up. You may still get coverage if your surgery was prophylactic and you chose to complete reconstruction. You could be asked to prove medical necessity though. The insurance department at the boutique will help you with this. However, if your provider does cover these, keep in mind that your deductible and co-insurance may still apply. Also, they may only cover “basic” bras, so no bejeweled magic lifting contraptions. 🙂

The topic of insurance coverage has come up a bit in the Facebook groups recently. There were some good questions. Having been through a few (ha!) surgeries, appealing rejected claims, and recently switching from one provider to another (United Healthcare > Blue Cross Blue Shield), I have a little bit of experience dealing with insurance and can share some thoughts and things to consider.

The topic of insurance coverage has come up a bit in the Facebook groups recently. There were some good questions. Having been through a few (ha!) surgeries, appealing rejected claims, and recently switching from one provider to another (United Healthcare > Blue Cross Blue Shield), I have a little bit of experience dealing with insurance and can share some thoughts and things to consider.

Well, as you already know,

Well, as you already know,